Key takeaways:

While useful, onchain metrics alone are insufficient for Bitcoin valuation, as a large portion of trading and ownership changes now occur off-chain. ETFs (holding 7% of supply), futures markets and macro conditions are now significantly driving Bitcoin’s price discovery as derivatives activity expands sharply. Valuing Bitcoin now requires a combined approach: analysis of flows along the chain in the future, such as ETFs. positioning, and macro liquidity signals.

For the first decade of Bitcoin’s existence, onchain metrics provided a reliable view of investor behavior and market cycles, as almost all trades and transfers took place directly on the blockchain. This valuation era came to an end in early 2024, when the introduction of US mock Bitcoin exchange-traded funds (ETFs) reshaped the market. Suddenly, offchain market data became a decisive factor, as investors were given an alternative entry point to the Bitcoin market. Although ETFs have sparked the need for a new era of Bitcoin valuation, futures markets and macro conditions also play a role. This shift raises an important question: Can onchain indicators still provide a clear picture of market conditions, or must they now be combined with offchain data to understand valuation?

How Bitcoin Valuation Worked Before ETFs

Before ETFs existed, almost all economic activity was visible on Bitcoin’s blockchain. With almost all the market activity available in one place, the following key indicators of Blockchain’s value were:

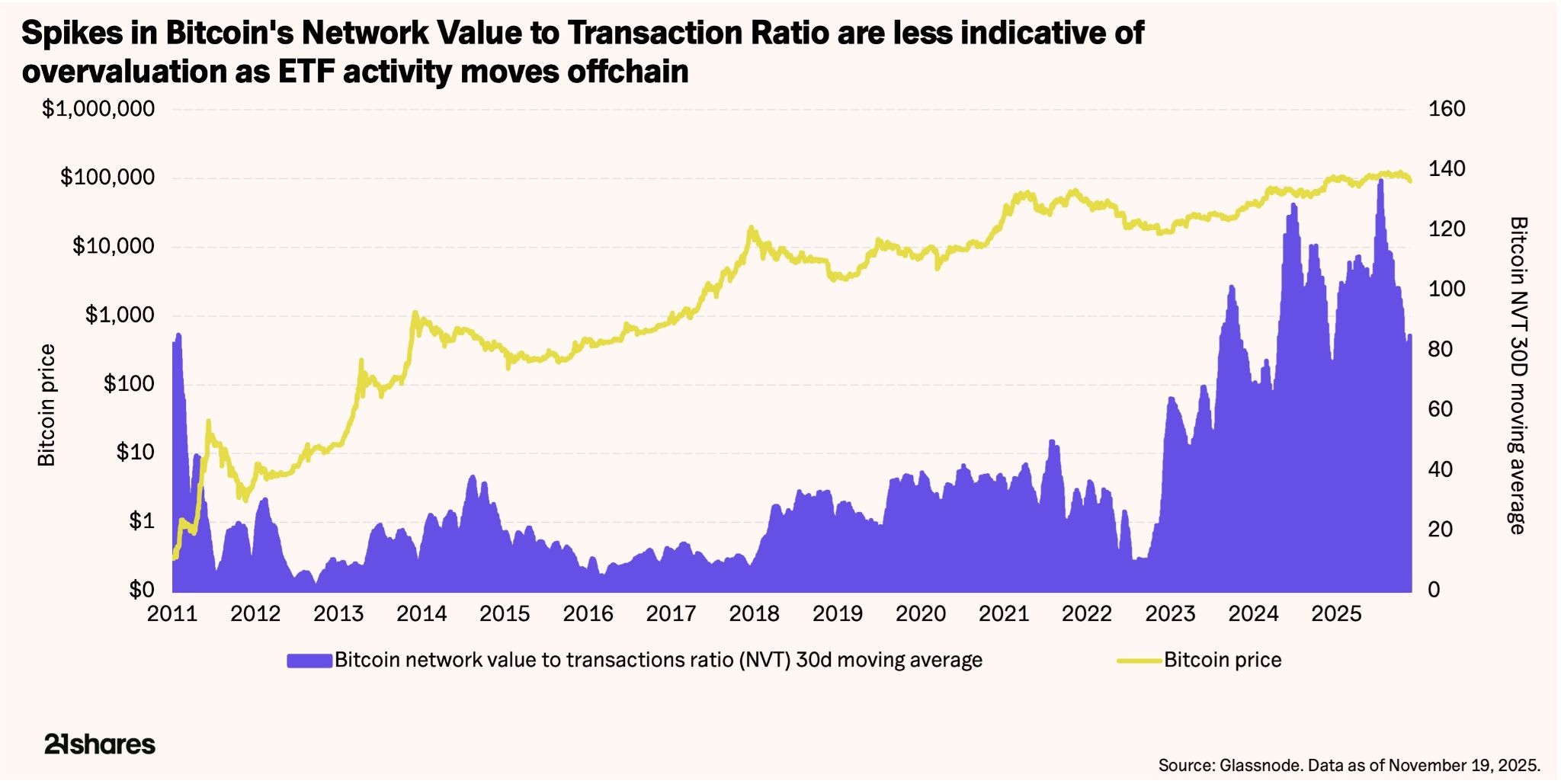

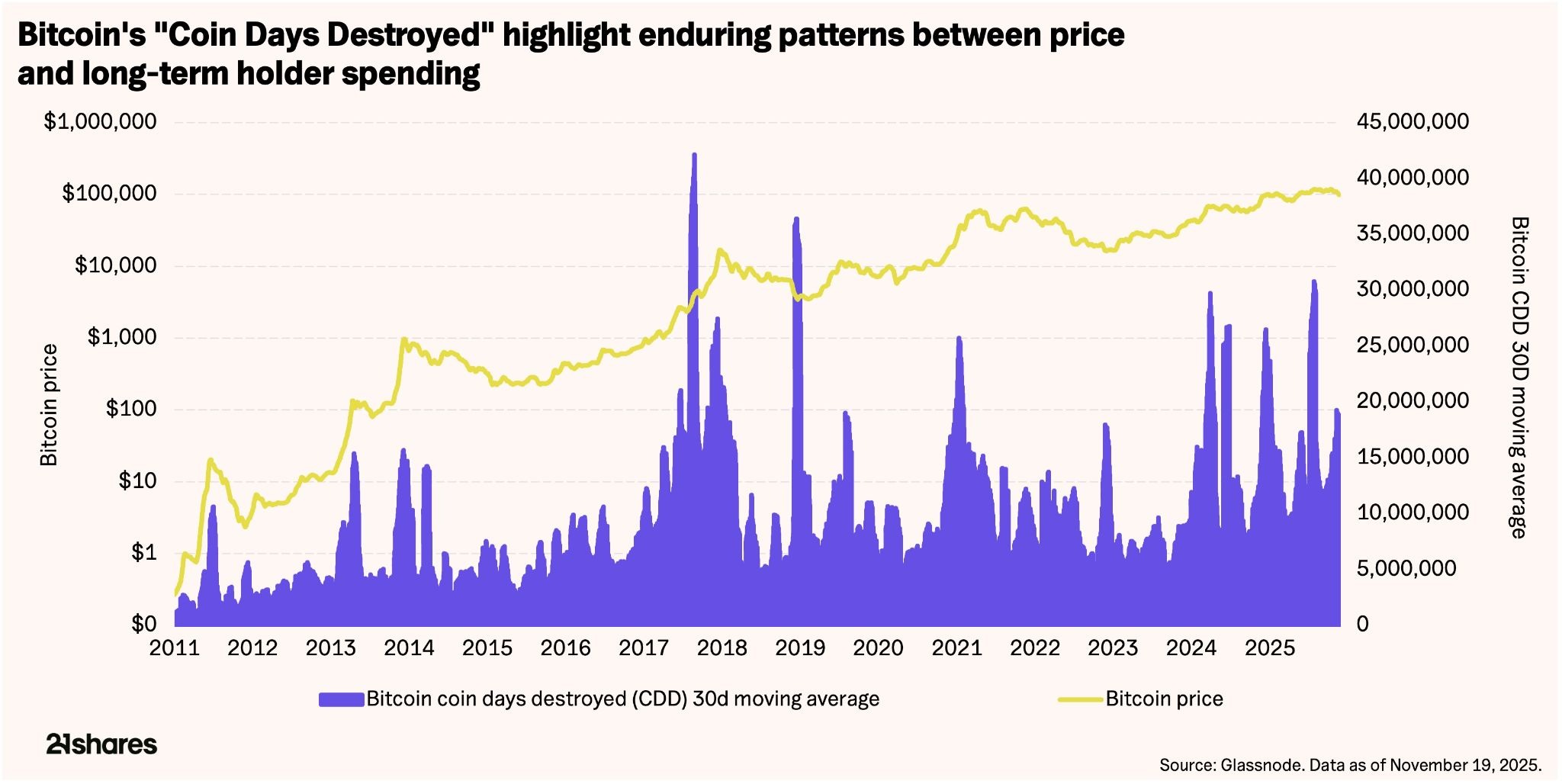

Market value to realized value ratio, which functions similar to a price to book ratio in traditional markets and is commonly known as MVRV. MVRV showed when the market was trading well above or below its total cost basis. Measures of unrealized profit and loss across the network, called Net Unrealized Profit or Loss or NUPL, also played an important role. NUPL captured periods of widespread optimism or stress. The Network Value-to-Transaction ratio, often shortened to N/A, acted like a Price-to-Earnings ratio by comparing the value of the network to the value of transactions moving across it. NVT spikes aligned well with cycle peaks and troughs by comparing the value of the network to the value transmitted. Coin Days Destroyed, or CDD, which is similar to long-term shareholder turnover, highlighted when long-held coins have been spent. Broader measures of activity such as active addresses, transaction counts and fee levels rounded out the picture, generally rising during expansions and softening before downturns.

How ETFs Changed the Market

The introduction of ETFs has changed the Bitcoin valuation landscape: large investors can now enter or exit positions through regulated funds, futures markets and custodial platforms that leave minimal onchain footprints. A significant part of supply and price discovery now takes place through off-chain instruments, such as spot and futures funds.

Since their launch in 2024, US spot Bitcoin funds have accumulated nearly 1.3 million Bitcoin, or about 7% of the total supply, held in custody.

At the same time, billions of dollars in Bitcoin exposure now trade on traditional exchanges without any blockchain activity, as shares of these products move between investors in the secondary market. Futures markets also expanded. Open interest reached record levels at the start of October 2025, allowing market participants to take large positions without moving any coins. Broader macroeconomic forces, including global liquidity conditions and interest rate policy, have also become more influential in shaping short-term price movements.

These developments mean that onchain data no longer reflects the full extent of Bitcoin economic activity. This is due to the growing migration of trading activities to offchain ETF markets, where secondary market transactions leave minimal onchain footprints. Note that active addresses peaked at 959K in March 2025 as BTC hit $70K, but ETF trading volume jumped over 150% from around $2B at launch to exceed levels of $4.5B2. Network usage declined accordingly: daily transactions dropped from nearly 500K in December 2023 to around 250K today, and the 30-day average transaction fees dropped from ~265 BTC before 2024 to just 4-7 BTC throughout 20253. This drop in onchain activity coincided with the traditional high idea, which Bitcoin reached at the same time. statistics no longer move in step with market value.

How traditional onchain metrics are performing today

Many of the traditional onchain metrics outlined above, especially those focused on transaction counts, fee levels, or basic N/A ratios, fall short of fully capturing the network’s economic throughput. While they still provide valuable context, they must be interpreted with the knowledge that a growing portion of Bitcoin’s use is mediated by vehicles that do not reside directly on the chain. Let’s take a look at three onchain stats and how they’re doing today:

The N/A ratio has become less reliable as so much activity now takes place outside the chain. Elevated readings don’t always indicate overvaluation as they once did, and updating the measure to include ETF trading volumes and flows will make it more accurate.

On the other hand, Coin Days Destroyed (CDD), Bitcoin’s closest equivalent to long-term shareholder turnover, has remained important because it highlights when long-dormant coins start to move. This often reflects distribution from early investors to new holders. Spikes in this measure continued to appear around market tops and bottoms, even after the introduction of ETFs.

Activity measures such as active addresses and transaction counts still help measure network health, but they are no longer strongly connected to short-term price behavior.

Getting a complete view of valuation now requires including both onchain and offchain signals together. The following three offchain indicators are key:

Daily inflows and outflows provide a short-term view of shifting sentiment (similar to onchain value transfers previously), with steady inflows reflecting strong demand and large outflows often consistent with risk aversion.

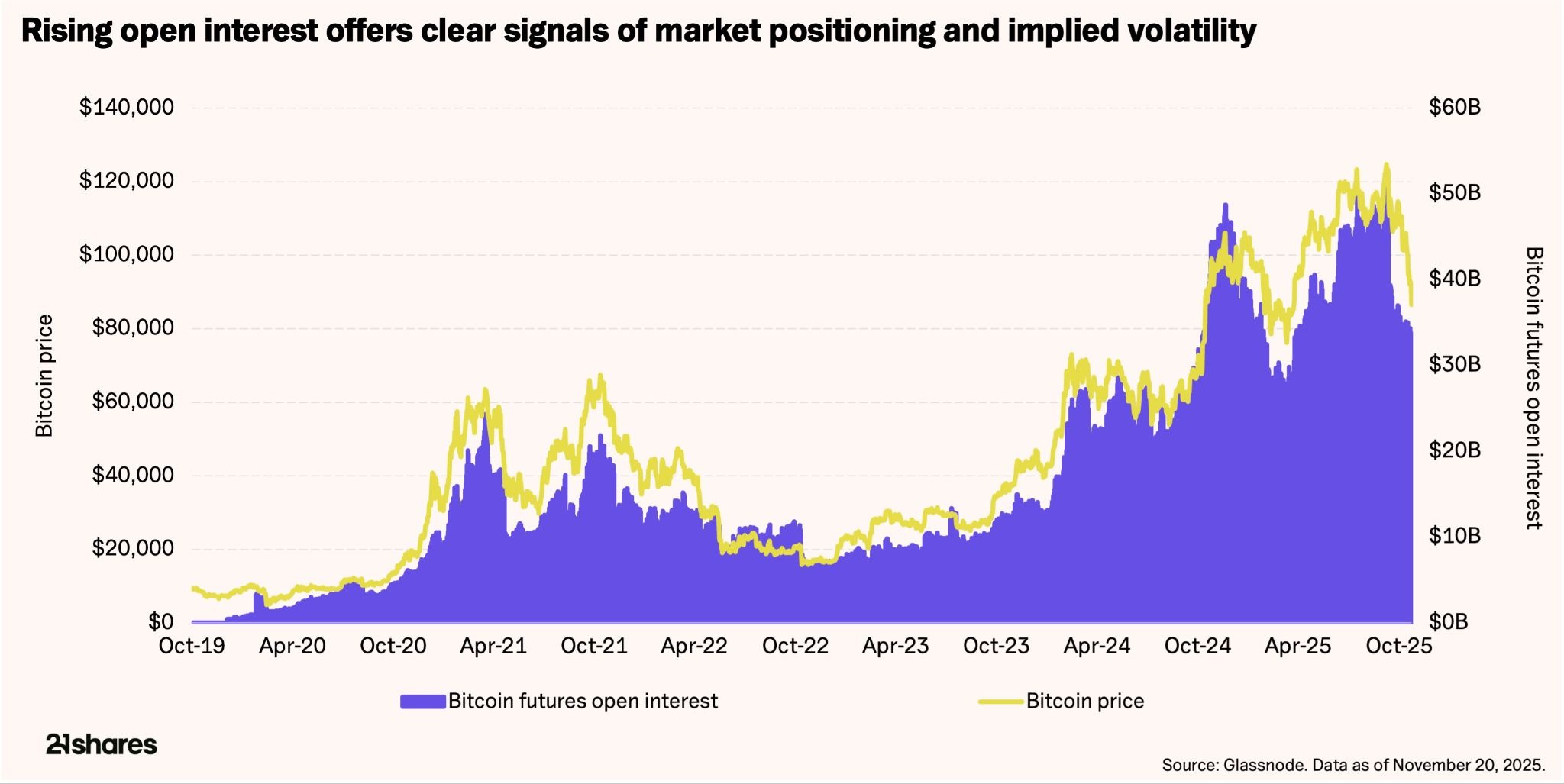

Futures market data adds important context, especially as the derivatives market’s open interest has grown roughly 500% since early 2020 and now represents a much larger portion of Bitcoin market structure. Rising open interest often signals upcoming volatility, while shifts in funding rates help show how the market is positioned. Most interestingly, open interest growth of 50-90% has preceded major volatility spikes (Oct 2020 – Apr 2021, Oct 2024 – Nov 2024, Apr 2025 – Oct 2025).

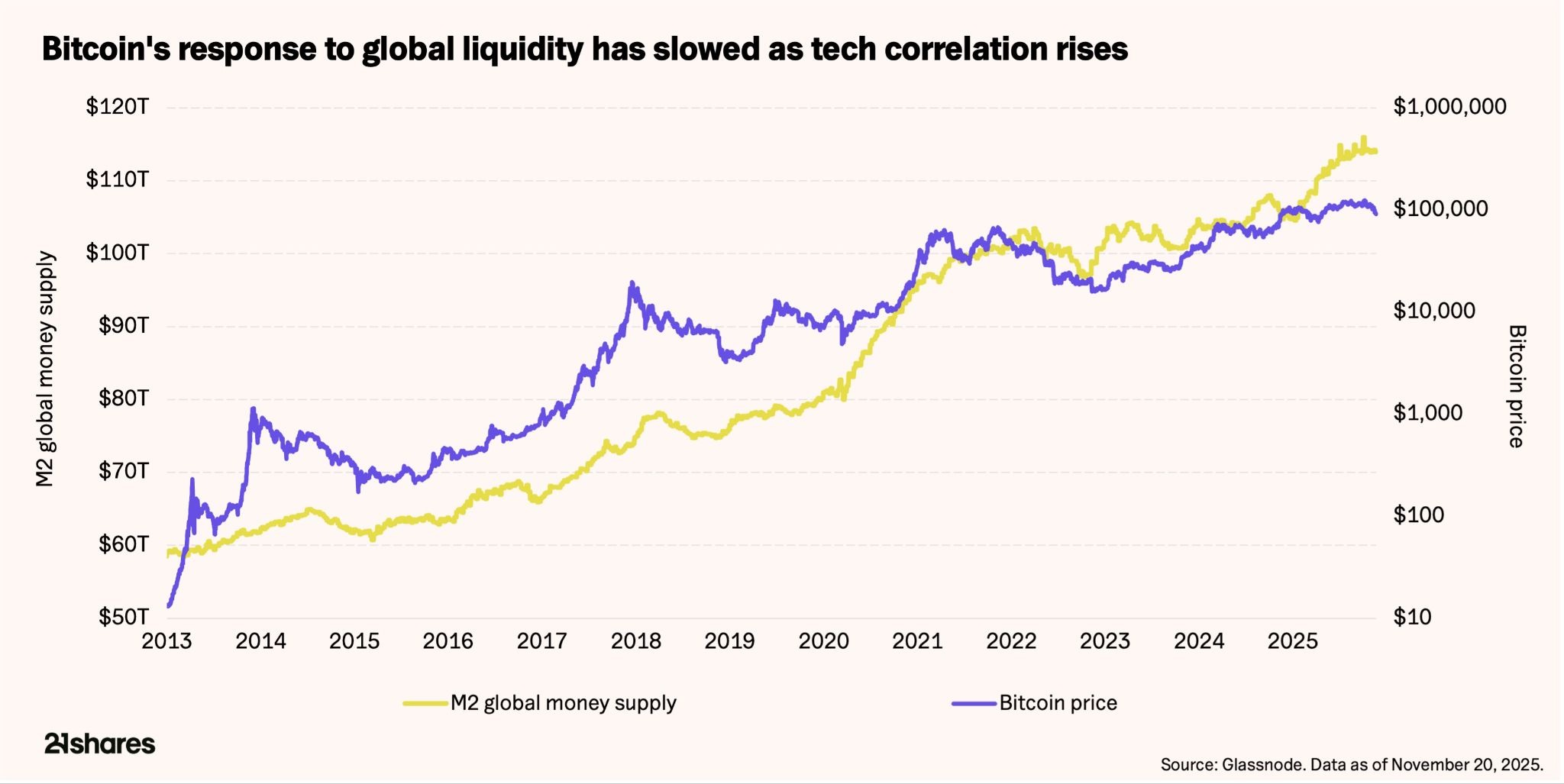

Similarly, macro liquidity measures such as money supply growth and real interest rates have also gained importance as Bitcoin behaves more like a global risk asset. Its increasing correlation4 with major stock indexes has amplified volatility and made it more sensitive to valuation changes in artificial intelligence-related and broader technology markets, which some see as overstretched.

All in all, onchain metrics still provide meaningful insight into cost base, investor behavior and long-term cycle trends, but they no longer provide a complete view on their own. With more inventory in repository and price discovery increasingly driven by ETFs and futures markets, a more integrated approach is needed. Combining onchain fundamentals with fund flows, derivatives positioning and macro conditions provides a clearer understanding of where Bitcoin stands in its evolving market cycle.

_____Footnotes: The Block. https://www.theblock.co/data/etfs/bitcoin-etf/bitcoin-spot-etf-volumesThe Block. https://www.theblock.co/data/etfs/bitcoin-etf/bitcoin-spot-etf-volumesGlassnode. https://studio.glassnode.com/charts/addresses.ActiveCount?a=BTC and https://studio.glassnode.com/charts/fees.VolumeSum?a=BTCNew Hedge. https://newhedge.io/bitcoin/bitcoin-correlations

Disclaimer for Uncirculars, with a Touch of Personality:

While we love diving into the exciting world of crypto here at Uncirculars, remember that this post, and all our content, is purely for your information and exploration. Think of it as your crypto compass, pointing you in the right direction to do your own research and make informed decisions.

No legal, tax, investment, or financial advice should be inferred from these pixels. We’re not fortune tellers or stockbrokers, just passionate crypto enthusiasts sharing our knowledge.

And just like that rollercoaster ride in your favorite DeFi protocol, past performance isn’t a guarantee of future thrills. The value of crypto assets can be as unpredictable as a moon landing, so buckle up and do your due diligence before taking the plunge.

Ultimately, any crypto adventure you embark on is yours alone. We’re just happy to be your crypto companion, cheering you on from the sidelines (and maybe sharing some snacks along the way). So research, explore, and remember, with a little knowledge and a lot of curiosity, you can navigate the crypto cosmos like a pro!

UnCirculars – Cutting through the noise, delivering unbiased crypto news